The role of ATM Technologies in the transition from traditional Banking to Digital Banking: The visible and invisible sides.

04.05.2026

Since the late 1960s, ATMs have undergone a long path of evolution, transforming from simple and convenient cash withdrawal machines into banking devices that deliver a wide range of digital solutions. Today, they meet the demands of both traditional and digital banking by providing financial technology services to economies that rely on cash as well as those that prioritize digital payments. Despite this, many people still perceive ATMs merely as cash withdrawal machines. The financial sector, in turn, often overlooks their broader potential as tools for delivering expanded solutions and building engagement with both existing and potential customers.

In this article, we will highlight the innovations reshaping ATMs, explore their contribution to achieving agility and inclusivity in digital banking, and clarify their effective role as a “bridge” between traditional and digital banking.

The Digitalization Journey of ATMs: Evolution

Today’s payment ecosystem is characterized by the coexistence of multiple participants and technologies. These include the use of cash, traditional card schemes (such as Visa or Mastercard), instant payments, digital wallets, QR-code-based payments, as well as increasingly innovative solutions such as payment platforms integrated into social networks and marketplaces. This diversity of participants and technologies makes the payment ecosystem dynamic, engaging, and continuously expanding.

As an essential component of the payment ecosystem, the true digitalization of ATM networks promises significant opportunities in terms of both customer experience and operational efficiency. This transformation is not limited to traditional ATMs; it also includes Interactive Teller Machines (ITMs), Video Teller Machines (VTMs), kiosks, and modern solutions such as Cash Pods. By delivering a broad spectrum of services in a changing financial ecosystem, today’s ATM devices can, to a large extent, be described as “bank branches.” The functionality of modern ATMs is no longer limited to basic operations such as cash withdrawals:

-

Card-based transactions: Using contact and contactless card technologies, customers can withdraw cash, access account information, and make bill payments through smartphones and payment cards.

-

Account-based transactions: Many ATMs now support QR-code functionality, enabling customers to initiate transactions via banking applications or e-wallets. This feature allows not only cash withdrawals from accounts, but also instant transfers and payments.

-

Account management: By completing KYC procedures, users can become bank or fintech customers, open accounts, apply for loans, place deposits, and update KYC information.

-

Cash deposit and recycling: ATMs equipped with cash recycling technology accept cash deposits, which later become available for withdrawals. This improves liquidity management and operational efficiency.

-

Financial literacy tools: Interactive guides help users manage loans, understand savings products, and make informed financial decisions.

Digital payments are rapidly evolving, and with them, cybersecurity and sensitive data protection have become critical necessities. These requirements are among the key criteria that modern ATM software and hardware infrastructures must fulfill.

-

Biometric authentication: Biometric solutions such as facial recognition and fingerprint scanning ensure that transactions are conducted in a secure environment.

-

AI-powered fraud detection: Advanced monitoring systems analyze user behavior patterns to detect suspicious activities, protecting both customers and service providers from operational and other risks.

Global Trends and Factors Driving ATM Innovation

Personalization and User-Centric Design

AI-powered algorithms enable ATMs to deliver personalized experiences. User interfaces can adapt to individual preferences and habits by offering frequently used services, preferred transaction types and amounts, and even customized language settings.

Sustainability and Green Banking

Leading ATM manufacturers are increasingly focusing on energy-efficient ATM solutions and implementing environmentally friendly components. Some machines are even produced using recycled materials, aligning the financial sector with global sustainability goals.

Balancing Cash, Card-Based, and Account-Based Payment Solutions

The future of payments lies in the harmonious integration of cash, payment cards, and QR-code-based solutions within a unified ecosystem that accommodates different user needs and experiences. Undoubtedly, contactless payments and QR-code functionalities will continue to expand.

Digital transformation is truly inevitable. However, it is important to remember that while the world is moving toward a “digital-first” approach, it is not becoming “digital-only.” Modernization and development are essential. Although society increasingly relies on digital channels such as mobile banking, not all regions have developed at the same pace, and the traditional ATM still remains a valuable part of the financial inclusion and self-service ecosystem.

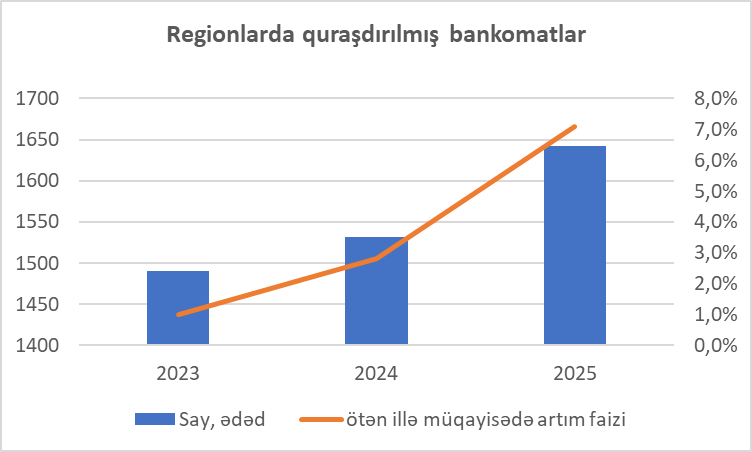

In recent years, the relatively slower growth of ATM numbers in Baku compared to the increasing dynamics in regional areas is therefore not surprising. In the regions, ATMs continue to be one of the most important components for ensuring people’s access to banking services.

Thus, by combining cash and digital payment instruments, ATMs will continue to serve as a bridge between traditional and modern banking. What matters most here is achieving a balanced position within the ecosystem. Why?

- Inclusivity: A hybrid system enables financially underserved populations to participate in the economy while also encouraging the adoption of digital payments whenever possible.

- Resilience: Maintaining cash payment capabilities alongside digital payment systems serves as an alternative during technological disruptions or emergency situations.

- Adaptability: Consumers can act flexibly by choosing between payment methods based on their preferences and circumstances.

- Cultural Sensitivity: Preserving balance and respecting cultural norms supports the adoption of innovation and facilitates changes in customer behavior.

Conclusion

The future of banking is not built on the choice of “either digital or traditional.” The future is shaped by integration, balance, and adaptability. From this perspective, ATM technologies are not remnants of the past, but rather one of the key pillars of the sustainable and inclusive development of the financial system.